Rebuilding the Foundations of US Offshore Wind

Ocean News

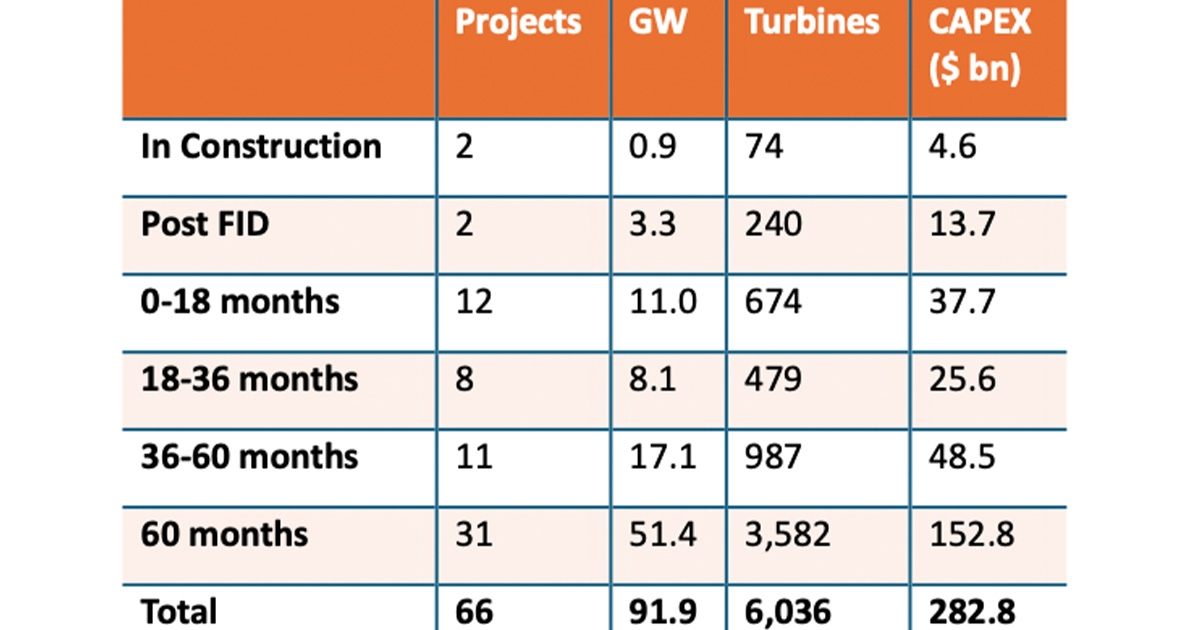

US Offshore Wind Opportunity by FID Timing. (Image credit Intelatus)

As we enter a New Year, the memories of the shocks to the foundations to the US offshore wind segment remain fresh. In short, supply chain inflation and capacity/availability, interest rate increases, and tax credit monetization have been the key themes highlighted by developers to explain why many projects became commercially unviable, as outlined in the most recent US Offshore Wind Report from business intelligence and consulting firm Intelatus Global Partners.

Several Northeast and Mid-Atlantic states have reacted rapidly, accepting the termination of power sales & purchase agreements and allowing the canceled projects to be rebid into new solicitations The Commonwealth Wind, SouthCoast Wind, Pack City Wind, Empire Wind 1 and 2, Beacon Wind 1 and Sunrise Wind projects, together representing more than 8.5 gigawatts (GW) of capacity, have either canceled or are expected to cancel power sales agreements and then rebid the projects into current solicitations for New York, Connecticut, Rhode Island and Massachusetts, which seek to commit as much as 9 GW of capacity, with contracts that provide some measure of price inflation protection. We anticipate that these projects will continue to be developed, but with a 6- to 12-month delay from the previous plan.

Ørsted has made a much-publicized announcement to cease development of the 2.3 GW Ocean Wind project, but the project retains value to be developed by a new party or even Ørsted as it is both permitted and has a secured offtake agreement. Again, we anticipate that this project will be developed at some stage more than five years in the future.

Several other projects in New Jersey and Maryland are also currently under review, where we see a risk of delay rather than termination.

Federal agencies continue to focus on project perming and advancing new leasing.

The Department of the Interior’s Bureau of Ocean Energy Management (BOEM) is preparing to lease two areas with a potential of 3.3-6.3 GW in Delaware and Chesapeake Bays in the Central Atlantic. Along with the Central Atlantic lease sales, BOEM is committed to leasing further sites in the Gulf of Mexico, Oregon, and the Gulf of Maine in 2024/2025. The cumulated capacity of the leases is estimated at 18.6 GW. When added to the potential capacity of those leases previously awarded, the total potential leased will amount to around 80 GW, of which close to 26 GW is at some stage in the federal perming process.

And it is not just federal agencies that are advancing offshore wind. The state of Louisiana has signed two leases in its waters for bottom-fixed wind farms with a combined capacity of 775 MW.

While federal and states agencies (re)build the foundations for future activity, first power have been generated from both Vineyard and South Wind, and Coastal Virginia is building up an inventory of monopiles in Portsmouth to commence offshore construction in the Spring of 2024.

We maintain our forecast of more than 65 projects that will install around 90 GW of capacity in this and the next decade and a total 110 GW by 2050.

The 90 GW forecast capacity will require capital expenditure amounting to around $283 billion to bring onstream, a recurring annual operations and maintenance spend of $9 billion once delivered, and close to $40 billion of decommissioning expenditure at the end of commercial operations.